Fresh pain for borrowers as Bank of England set to increase interest rate for the 13th time in a row

An interest rate rise by the Bank of England at midday is a nailed-on certainty – though opinions are split on the level of additional pain that could be imposed as efforts to curb the country’s inflation problem stumble.

At the start of this week, policymakers were widely tipped to raise the base rate by a quarter of a percentage point to 4.75% – a record 13th consecutive increase – maintaining a slower path for hikes since March.

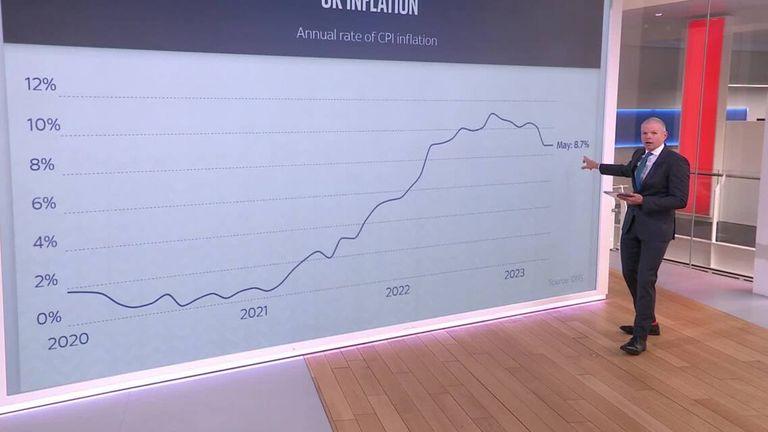

But the latest inflation figures, published yesterday, prompted financial market participants to anticipate a greater, almost even, chance of a half percentage point hike to 5%.

While there were already concerns about the stubborn pace of price rises, the inflation data came as a shock.

It showed price growth was becoming more engrained in the economy while the main consumer prices index (CPI) also failed to budge lower as most experts had predicted.

The Bank had also previously expressed concerns about the pace of wage rises which, it argues, contributes to demand and further inflation ahead.

Inflation is proving more difficult to cool than had been anticipated, and Chancellor Jeremy Hunt told Sky News last month he would even be comfortable with a recession if it brought inflation to heel.

The only tool the Bank has to do that, rate rises, will mean more pain for borrowers whatever today’s rate decision brings.

Read more: PM and chancellor face conundrum as mortgages rise – and there’s no silver bullet to end the crisis

Growing interest rate expectations over recent weeks have forced up funding costs for lenders, with data from Moneyfacts this week showing average rates for two-year fixed mortgage deals rising above 6%.

They have continued to rise each day this week having stood just above 2.5% in March last year.

With the financial markets now seeing the Bank rate potentially rising to 6% by early next year, such a level, if realised, would mean mortgage rates have far further to rise.

Read more:

The solution to bringing down inflation is a political nightmare for the Tories

Mortgage misery: What is causing the crunch, will it get worse and what can you do if you are struggling?

‘Eyewatering’ hit to 1.4 million, mainly young, mortgage customers ahead, IFS warns

In making its rate decision today, the Monetary Policy Committee could face a big split in voting – though the majority of opinion among commentators is that a quarter-point rise will be the result.

After all, the Bank has consistently steered markets away from their peak rate scenarios this year and even signalled that a pause in the rate cycle was close.

But the core function of the MPC is to keep inflation around a target rate of 2% – and there are signs of frustration in Whitehall that the independent Bank of England is lagging behind the curve.

So at a sticky 8.7% – and with wage growth and so-called core inflation (which strips out volatile elements such as energy and food) ticking up last month – some might be forgiven for thinking there was every justification for a 0.5 percentage point rate hike.

‘Sticky’ inflation explained

The other side of the argument suggests a smaller rise would be sufficient as there is evidence that the 12 rate hikes to date, along with a natural easing in many costs, were starting to have an effect.

Samuel Tombs, chief UK economist at Pantheon Macroeconomics, said wider data suggested wage growth pressures would start to reduce and that energy-linked inflation would fall sharply, allowing an easing of price growth more widely.

He said of the MPC’s dilemma: “The headline rate of CPI inflation still looks set to fall sharply over the remainder of this year, probably to about 4.5% by December and to around 2% in the second half of 2024.”

He added: “We continue to think that the MPC will not raise Bank rate all the way to the near 6% level priced-in by markets before today’s data; for now, our base case remains Bank rate peaks at 5%.”

For all the latest business News Click Here