He’d joined Morgan Stanley in the grim days of 2009, when big banks were trying to pay back taxpayer bailouts and deflect public fury. But four years later, the ire was fading and ambition was the order of the day.

“It really felt like, for the first time, the job and the career weren’t defined by the context of the financial crisis,” Diop said. “We are past this now. And now it’s time for us to do new deals.” In the years that followed, his rise to managing director traced a new boom. He helped orchestrate a multibillion-dollar deal with SoftBank Group, whose breakneck investments defined an era, then closed a huge SPAC merger at the height of that rush.

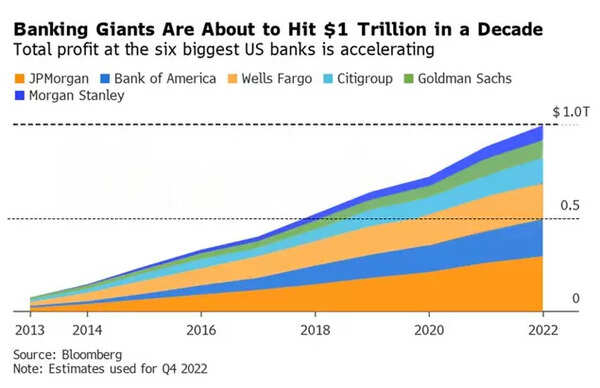

Diop didn’t know it, but he was playing a small role in something almost unfathomably lucrative: The first trillion-dollar decade for the six giants of US banking. That’s not $1 trillion of total revenue, it’s pure profit.

Such a haul didn’t seem possible before the decade began, when Wall Street was the target of a global protest movement and politicians at both ends of the spectrum were seething over bailouts or aiming to break up too-big-to-fail lenders.

They swelled instead, outpacing corporate America so handily that JPMorgan Chase & Co, Bank of America Corp, and even hobbled Wells Fargo & Co are on track to make more profit over those 10 years than all but a few publicly traded US companies, according to data compiled by Bloomberg.

Citigroup, Goldman Sachs Group Inc. and Morgan Stanley aren’t far behind. And together the six are poised to make even more next year.

While much of the world’s attention was focused on the riches minted by Silicon Valley, banks were gaining momentum. There isn’t one way to explain how they pulled it off: Volatility juiced Wall Street’s trading hauls, investment bankers like Diop rode a dealmaking boom, and Donald Trump boosted bottom lines by slashing taxes. Likewise, there isn’t one reaction across the industry to the milestone.

“Sometimes there’s this sense that the fact that they profited that much is somehow terrible, and I just don’t think that’s the case,” said Betsy Duke, a former Federal Reserve governor who chaired Wells Fargo’s board until 2020. “About everything you could throw at the financial system has been thrown at it in the last 10 years. These banks have not just survived but they’ve actually thrived.”

In a decade of public anger at the banks, tougher rules, geopolitical havoc, the pandemic and some treacherous market swings, banks “were able to cope with all of that, and not only cope with it but earn $1 trillion,” Duke said.

Analyst estimates show the six banks are quickly closing in on that feat — $1 trillion in a 10-year period — and that if they don’t reach the milestone at the end of this month, they will sometime in the first few weeks of 2023. It isn’t just the scale of profit that’s so startling, though, but the industry’s ability to push through scandals and thrive anew.

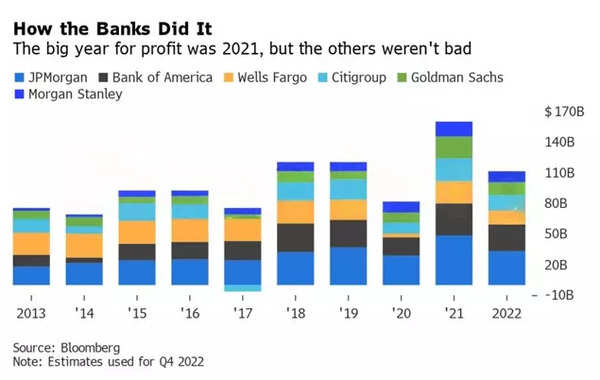

Ten years ago, JPMorgan, now the most profitable and valuable US bank by market capitalization, was in the doghouse after the London Whale trading fiasco. Wells was on top of the big six, the most valuable and the sole member of the group pulling in more than $20 billion. Though its earnings were later derailed over revelations of consumer abuses, analysts see it nearing that level again in 2023.

What didn’t transform over those years is the broad outline of the business: Banks sell stocks and bonds, trade financial instruments, advise on corporate takeovers, manage wealth, handle payments and lend. Back in 2013, some traders were already mourning the casino-style risk-taking that Dodd-Frank of 2010 threatened, even if Washington was still hammering out the exact rules.

Paying for scandals

To get out of the shadow of the global crisis, the banks had to pay. In 2014, Bank of America agreed to a record-breaking $16.7 billion settlement to end probes into shoddy mortgage practices, passing JPMorgan’s $13 billion. By then, some banks were mining new veins of profit that got them into trouble.

Employees inside Wells Fargo, under pressure to meet sales targets, set up millions of accounts for customers who hadn’t asked for them, the most famous in a series of scandals that ultimately spanned most of its businesses. And in Malaysia, Goldman Sachs finished raising billions of dollars in 2013 for a state-owned investment fund known as 1MDB, which was then pilfered by a group including the former prime minister.

“My biggest regret in the last decade was not stopping the 1MDB transaction,” said former Goldman partner Robert Mass, a compliance executive. “Each issue was vetted, in some cases multiple times, but in the end the answers that we received satisfied us.” Mass, who now teaches philosophy at Hunter College in New York, said the firm was “misled by our own people, who were in on the bribe, in a way that we had no reason to doubt and could not disprove.” He wasn’t sure if he learned any lessons, “other than to be less trusting.”

The magnitude of profit makes those mistakes look like hiccups. One person the industry can thank, Trump, taunted banks on the campaign trail before putting two Goldman alumni in charge of a tax overhaul that helped transform corporate profits. Banks that had gotten used to paying three in ten dollars to the government found themselves forking over less than one in five for 2018. Their tax bills went down from there.

That year marked a new intensity for Wall Street’s growth. Banks that had made less than $70 billion in 2017 made $120 billion in 2018 thanks to tax cuts, an uptick in interest rates and surges in retail banking and dealmaking. Their combined assets, which hovered around $10 trillion for years, began to shoot up.

The way top Wall Street lawyer H Rodgin Cohen sees it, all of this shouldn’t be a surprise. “Banks may be seen as always winning with a couple of exceptions because of their role in the economy,” said Cohen, who’s now senior chair of Sullivan & Cromwell LLP. “They are intermediaries. They’re borrowing and they’re lending.”

The decade was a frothy time to be a banker. Personnel expenses for the six companies, which had hovered around $148 billion at the beginning of the era before dropping for a few years, jumped to $154 billion in 2019, never mind that their overall number of employees had actually fallen. Jamie Dimon, the JPMorgan boss who’d already become a billionaire, would eventually get such a big pay package that a proxy advisory firm told shareholders to vote against it.

“One of the goals of a good society is that everyone, including those people at the bottom, have enough to survive and flourish,” said Mass, the former Goldman partner who now studies ethics. “I am OK that people are paid well for producing products and services that increase the overall level of wealth in society, but only when we combine that with appropriate taxation and sufficient social safety so that those at the bottom can flourish.” He added that he isn’t enough of an expert to say if current taxes and safety nets are the right size.

Few things transformed the landscape of Wall Street as profoundly as the pandemic’s arrival in 2020. To avoid economic cataclysm, the government rolled out relief programs for consumers and businesses, and the Fed bought trillions of dollars of assets. The market mayhem brought back the volatility that trading floors crave. Corporations lined up to borrow, raise capital or buy weakened competitors.

Things were changing inside the banks, too. When police murdered George Floyd that May, Diop found himself inundated with messages from classmates and colleagues.

“It was from an actual good place and well meaning, but at the same time you get 20 of those calls because you are the lone person that comes up,” he said. It was “exhausting to be everyone’s Black friend at that moment.”

That September, the news that Jane Fraser would become the first woman to run one of the big US banks was greeted by her colleagues with cheers, but also frustration for how long it took.

“I tried to change the industry from the inside out at the three largest banks and I failed — I have the shards of glass on my head to show it,” said Anne Clarke Wolff, a former executive at Citigroup, JPMorgan and Bank of America who founded Independence Point Advisors last year. “In 10 years at a big bank, the CEO didn’t spend 10 minutes with me — and I was among the most senior women.”

In early 2020, analysts were writing obituaries for Wall Street’s run of record profits. Instead, the banks helped spark the boom of blank-check companies known as SPACs. Later, once regulators got jittery and prices soured, investors were left holding the bag.

Profits in 2021 also got help from an accounting move: The banks felt good enough about the economy, thanks to government intervention, to release some of the reserves they had set aside in case loans soured. The big six made more profit in 2021 than in 2013 and 2014 combined. Even when Russia invaded Ukraine this year, the chaos helped traders defy expectations of hard times.

The tally of profits from the past 10 years eclipses the prior decade’s even if you take into account inflation and big bank mergers during the financial crisis.

Yet other corporate titans, especially in Silicon Valley, did too well for Wall Street to claim a monopoly on success. Apple Inc. alone made more than half a trillion dollars. Microsoft, Berkshire Hathaway and Alphabet topped JPMorgan, followed by Exxon Mobil edging out Bank of America and Wells Fargo.

Banks would attribute some of their gains to innovation, after they invested in tech platforms and improved offerings including credit card rewards. They’ve also helped companies tap capital markets to grow the economy. And they’ve held on to some of the profit, adding more than $200 billion to their capital buffers over the past decade to make a repeat of 2008 less likely.

Critics would counter that the banks didn’t do it alone. Many of them wouldn’t have survived 2008 if it weren’t for taxpayer aid, and those buffers are the result of stiffer capital rules, sometimes enacted over bankers’ strident objections. Moreover, it was another government intervention that propped the economy up during the pandemic, teeing up those record profits. Among other knocks: Some banks have focused on a narrower slice of clients, limiting opportunities for many communities, and have been slow to pass along rate hikes to savers, betting that customers won’t flee to smaller rivals.

Ultimately, banks’ fortunes depend on the health of their clients, Cohen said. Their epic profits will drop “if the economy takes a downturn, a real downturn,” he said.

Diop’s career shows the potential pitfalls. Two major mortgage companies he helped bring to the public markets during the pandemic are down more than 50%, battered by higher interest rates and economic concerns.

Even when markets were ebullient, Diop worried about how things would look when the mood turned. “But you can’t be on the sidelines for every deal,” he said. This year, he left Morgan Stanley to become an executive at Hoorae, the media company run by the actor and producer Issa Rae, his sister.

“I actually already miss it a little bit,” he said. “I miss figuring out what’s next.”

For all the latest business News Click Here