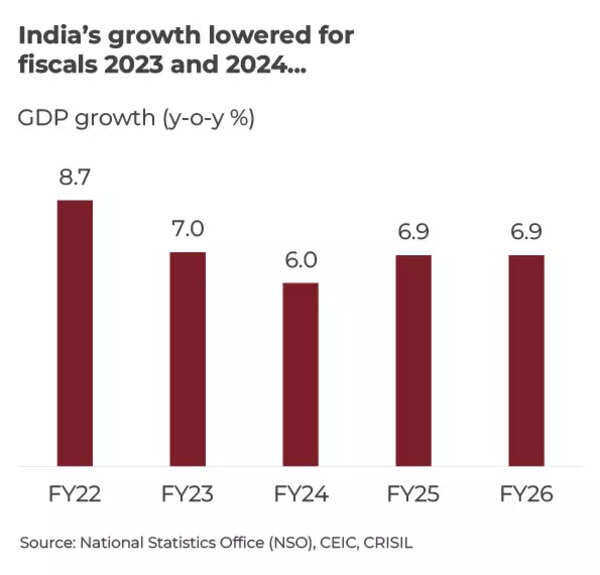

According to an analysis by Crisil Ratings, India’s GDP growth will slow to 7% in fiscal 2023 and 6 percent in fiscal 2024 as global growth decelerates faster. Additionally, domestic demand could come under pressure as interest rate hikes gets transmitted more to consumers, and the catch-up in contact-based services fades.

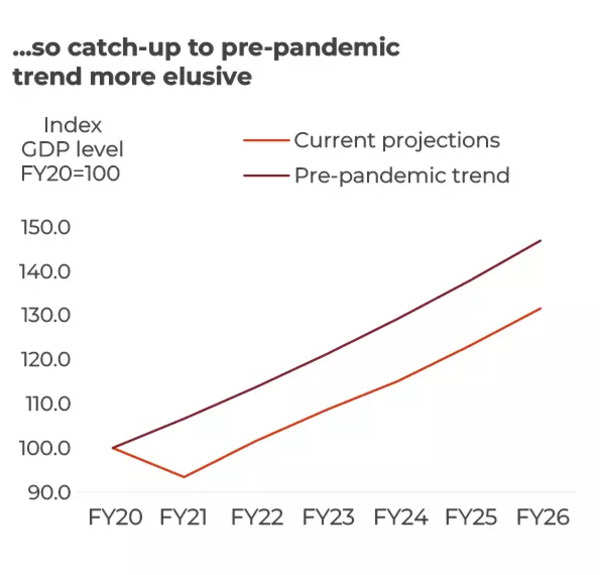

India’s growth lowered for fiscals 2023 and 2024… …so catch-up to pre-pandemic trend is more elusive

We explain in detail the factors that will contribute to this slowdown:

1. Global slowdown to impact domestic industrial activity via the exports channel

As central banks aggressively raise rates to fight inflation, advanced countries will find it hard to stave off a sharp downturn in activity. According to S&P Global, global growth is set to decline from 3.1% this year to 2.4% in 2023, led by slower growth in advanced economies, especially eurozone and the United States (US).

In the base case, S&P Global expects a shallow recession in the US in early 2023 while Eurozone is expected to grow a mild 0.3% in 2023, markedly down from the 3.1% forecast for 2022.

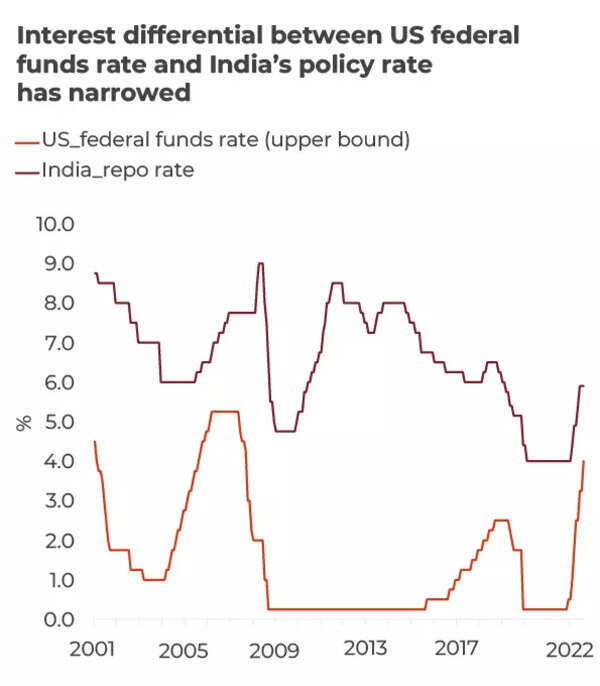

The US Fed has raised rates by 375 bps cumulatively (as of its latest November meeting). Aggressive monetary tightening in the US this year has meant the interest differential between the US federal funds rate and India’s repo rate has narrowed to around 190 bps, much lower than the pre-pandemic five-year average of 450 bps. This narrowing of interest rates has led to concerns over outflow of foreign funds, which may consequently increase the depreciating pressure on the rupee.

Though a weakening rupee supports exports to some extent, it is overshadowed by the impact of slowing demand, which is a dominant influencer of export growth

Monetary policy tightening and weakening growth momentum in advanced economies have already started to impact India in the form of slowdown in exports and volatility in foreign portfolio investment (FPI) inflows.

Not only have merchandise exports come under pressure, some of the services exports (related tourism, etc) and remittances could face headwinds from the growth slowdown in the advanced economies.

“The impact of tightening will be more pronounced next fiscal because monetary policy actions manifest with a lag. India’s core (non-oil, non-gold) exports declined by a massive 16.9% on-year in October; core exports have declined for three consecutive months now, with an average decline of 7.8% between August and October. The economy also witnessed net FPI outflow averaging $0.4 billion in September and October after an average inflow of $3.7 billion in the previous two months,” said Dharmakirti Joshi, Chief Economist at Crisil.

2. Industrial activity in India has begun to feel the tremors

India’s exports (particularly non-oil) have been slowing since July 2022. India’s exports have reduced significantly to the US (0.4% on-year in September versus 28.7% in June) and the European Union (EU) (2.8% vs 38.9%), noted the report.

Falling exports have affected domestic industrial momentum. Index of Industrial Production has been on a falling trend since July 2022 for export-linked sectors.

“The hit to industrial activity could intensify in fiscal 2024, as aggressive rate hikes in the US and the EU reach closer to consumers. Yet, rising domestic demand in some pockets has been partially cushioning industrial activity. For instance, robust government capex is supporting manufacturing growth through higher demand for infrastructure and construction-related goods,” said Joshi.

The global slowdown’s hit to Indian exports could also weaken income prospects in the labour-intensive manufacturing industry such as textiles, and gems and jewellery.

However, the overall impact could be less pronounced this time because the China-plus-one policy ( a global strategy in which companies avoid investing only in China and diversify their businesses to alternative destinations) will gradually turn more export demand towards other economies, including India.

3. Household demand holding up this fiscal, helped by services catch-up and government capex, but will moderate next fiscal

Consumer spending is growing for some goods and services but also declining for others. While passenger vehicle sales have been recording double-digit growth since May 2022 and have crossed pre-pandemic levels, two-wheeler sales continue to wallow below corresponding levels. Even consumer non-durables have been recording their sharpest decline in growth among major IIP components since March 2022.

Passenger traffic is logging double-digit growth for both rail and air traffic, but a lot of the robust pick-up in services can be explained by the pending catch-up to pre-pandemic, said Crisil.

Core imports have been on a slowing trend in September-October 2022. IIP has also been declining for consumer durables and non-durables, possibly reflecting weakening demand conditions.

4. Weather sway over rural demand

Rural income prospects has been dependent on the vagaries of weather. Agriculture production was impacted by unusual weather events this year. First, there was the heatwave in March-May, which damaged the wheat crop at its harvesting stage. Then came delayed rains that hurt sowing of the rice crop. And finally, excess rains in October hit several kharif crops at the harvesting stage. While India saw excess rains in October last year as well, their quantum and duration was relatively higher in 2022.

“For this fiscal, we see agricultural GDP growth a tad slower at 3.0% compared with the decadal average of 3.8%. Heathy soil moisture and reservoir levels will support agriculture in the rabi season, which should offset some of the damage to kharif crops from erratic rains,” said Joshi.

Increasing extreme-weather events highlights a bigger challenge. And, while lowering of demand for MGNREGA jobs is an encouraging sign for rural economy from a job perspective, depressed wages are a matter of concern for rural demand.

5. Tighter financial conditions could test resilience of domestic demand next year

So far, the Reserve Bank of India (RBI) has raised the policy repo rate by 190 basis points (bps). While the repo rate is higher than the pre-pandemic level of 5.15%, it is lower than 6.50% peak reached in 2018 during the last rate hike cycle. Similarly, bank lending rates are lower than the pre-pandemic five-year average so far, implying that the impact on domestic demand and lending activity, is still not adverse. But this is expected to change soon as transmission of rate hikes and lower liquidity to the system is picking up. “As transmission increases, higher borrowing costs could take some steam off from the current strength in domestic demand,” said Crisil.

6. Risk factors to inflation this year

In the first half of this fiscal, consumer price index-based inflation has remained elevated at 7.2%, above the RBI’s upper tolerance band of 6%. This was due to a combination of factors, largely supply-led, both domestic and global:

• Surge in food inflation at the start of the fiscal due to the heatwave’s impact on foodgrains and vegetables

• Uneven monsoon distribution/ delayed monsoon withdrawal impacting sowing and harvest

• Pass-through of input prices to consumers, especially in sectors that saw demand revival (services)

• Elevated food and international energy commodity prices driven by geopolitics (crude oil, natural gas, fertilisers) and/or supply constraints (coal, metals)

Risks for the remaining of the year

• Tight wheat supplies will continue to contribute to higher cereal inflation until the rabi season. Further, despite rice buffers, lower rice kharif sowing is leading to increased prices for the crop

• Delayed monsoon withdrawal and seasonal demand would mean vegetables would see elevated inflation till November. Already, in October, retail prices of onions and tomatoes have risen in double digits on-year

• Persisting geopolitical tensions impacting international energy prices

For the full fiscal, Crisil expect CPI inflation to average 6.8% on-year.

Amidst all this gloom, there is a silver lining!

Despite the markdown in near-term growth, India is expected to remain a growth outperformer over the medium term as Crisil expect India’s GDP growth to average 6.6% between fiscals 2024 and 2026, compared with 3.1% globally — as estimated by the International Monetary Fund (IMF).

India is also likely to outgrow emerging market peers such as China (4.5% growth estimated in calendar years 2023-2025), Indonesia (5.2%), Turkey (3.0%) and Brazil (1.6%).

What are the reasons for this, according to Crisil?

Stronger domestic demand is expected to drive India’s growth premium over peers in the medium run

Investment prospects are optimistic given the government’s capex push, progress of Production-linked Incentive (PLI) scheme, healthier corporate balance sheets, and a well-capitalised banking sector with low nonperforming assets (NPAs).

India is also likely to benefit from China-plus-one policy as global supply chains get reconfigured.

Private consumption will play a supportive role in raising GDP growth over the medium run.

For all the latest business News Click Here