The market turmoil caused by Friday’s seismic mini-budget has hit mortgage offerings as providers withdrew partial and entire lending ranges.

Virgin Money and Skipton Building Society have temporarily withdrawn their entire mortgage product range, while Halifax, the country’s largest mortgage lender, said it is to remove fee-paying mortgages.

Fee-paying mortgages allow borrowers to pay a fee in exchange for a lower interest rate.

Britons warned of 6% interest rates – live updates

Halifax’s changes are to take effect on Wednesday, while the Virgin Money and Skipton Building Society decisions have already taken effect.

Chancellor Kwasi Kwarteng’s announcement of the most extensive programme of tax cuts for 50 years, and the associated market upset, has traders expecting that the Bank of England will raise interest rates to 6% – even higher than it outlined last Thursday.

On Monday, the Bank fuelled those fears when, in a surprise statement, it said it “will not hesitate to change interest rates as necessary”.

That uncertainty around the future of rate rises has caused the withdrawal, one broker told Reuters.

“The uncertainty around the risk of an emergency rate rise is likely to see other lenders withdrawing products or increasing rates dramatically until they know the extent of how this all pans out,” Jamie Lennox, a director at Dimora Mortgages, said.

Read more:

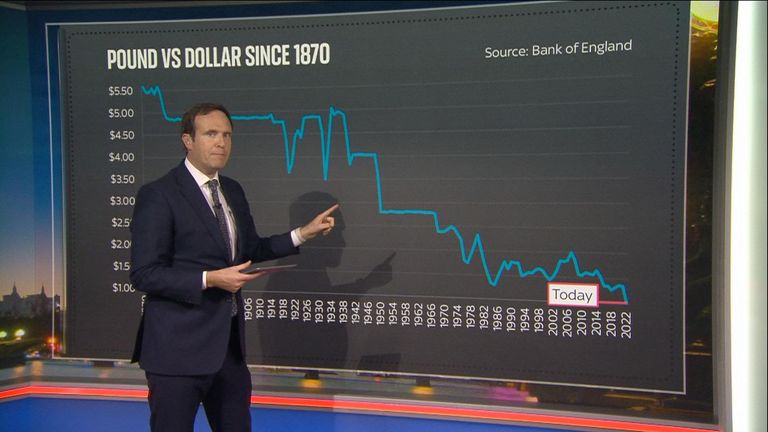

Five reasons why pound’s ‘doom loop’ matters to you

Could mini-budget bankrupt UK? Your questions answered

Why has the pound fallen to a record low?

Parent company Lloyds said Halifax was making the changes to its mortgage product offering “as a result of significant changes in the cost of funding”.

Virgin Money made its decision “given market conditions”, a spokesman said in a statement, with already submitted applications to be processed as normal.

The provider said it hopes to launch new products towards the end of the week.

For all the latest business News Click Here