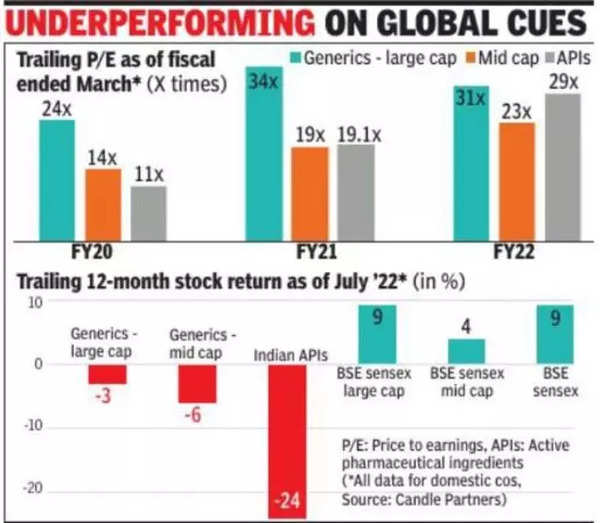

As against this, the BSE sensex delivered about 9% return (see graphic), said an analysis by investment banking and advisory services firm Candle Partners. Over the last year, M&As worth around Rs 4,000 crore have been executed and, based on media reports, deals worth Rs 6,000-7,000 crore are in the pipeline, with companies including Medley Pharma, Curatio Healthcare and Maneesh Pharma on the block.

The lacklustre show is being attributed to an overall low sales growth, flat US businesses, and low RoCE (return on capital employed) of 11-13% range over the last five years, as well as a deteriorated working capital cycle. “Domestic formulations sector has been a safe haven for both industry players as well as private equity investors as consistent growth & high ROCEs & margins are a sharp contrast to several regulated market businesses, where millions of dollars have gone in and returns are questionable,” Candle Partners founder Navroz Mahudawala said.

The flat/negative growth of US businesses is possibly the single biggest factor for the bearishness of the stock markets. The US is the most lucrative market for generic companies, contributing the largest — about one-third — to overall revenues. Major companies like Lupin, Zydus, Glenmark and Wockhardt have been facing headwinds due to the pricing challenges. Pricing pressure in the US on generic drugs dented the profitability margins for large- and mid-cap companies. While ebitda margins peaked at 28% in FY14, it is now around 21%.

All large caps, excluding Sun Pharma and Cipla, have given negative returns over the last 12 months with several of them having declined over 40%, the study says.

Over the past few years, revenues from the US market have grown at a relatively modest pace, reflecting multiple challenges faced by companies in the form of consistent pricing pressure, lack of major generic product launches and increased regulatory scrutiny. Rating agency ICRA’s VP & co-group head Kinjal Shah said in a note recently, “Off late, Indian pharmaceutical companies have reported sizeable provisioning and settlement payouts against some of the ongoing litigations, which have impacted their earnings and balance sheets to an extent. Indian pharmaceutical companies remain exposed to regulatory risks arising out of regular scrutiny by US regulatory agencies.”

Over a five-year period, the sector posted a revenue growth of 7%. If the companies that have grown through the inorganic route are removed, the growth rate of several large companies is in low single digits, the analysis says. The US sales as a percentage of total formulations peaked at 42% in FY17 and since then there has been a consistent decline. The decline of US revenues in the sales mix has been mainly compensated by India revenues (up from 27% to 32%) and rest of the world (RoW) markets (20-23%), it adds. Understandably, most domestic companies like Cipla, Dr Reddy’s and Lupin have started re-focusing on their India business, and other emerging markets.

India and RoW growing 10-12% have been the key positives for the industry, which has helped in mitigating the US performance. On the back of successes of the likes of Dr Reddy’s and Lupin, several mid-sized pharma companies had invested in the US as a geography in 2013-2018. Learning from underperformance of even the biggies has made several companies refrain from undertaking fresh investments in the US, it adds.

For all the latest business News Click Here